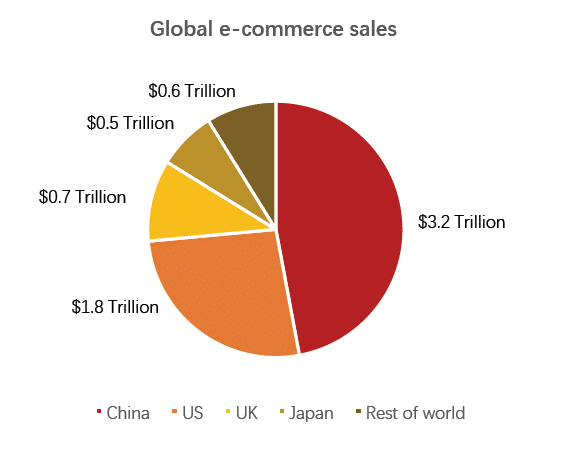

Shoes off. Phone in hand. A few idle taps, and groceries, dinner, or an impulse buy you didn’t know you wanted are already on their way. Multiply that moment across hundreds of millions of consumers and you have the Chinese B2C e-commerce market, which is projected to soon surpass $3.2 trillion in sales – nearly half of global online retail revenue. Against this backdrop, the question facing shopping malls is no longer whether they can compete with digital platforms, but rather how to reinvent themselves to remain relevant in an era defined by effortless and ever-available digital consumption.

A SIGNAL OF WHERE MALL LEASING IS HEADED

Parkway Health recently opened a flagship location inside Shanghai Plaza, a centrally located mall on Middle Huaihai Road. The facility is comprised of six medical centers, offering primary care as well as specialist consultations over more than 20 departments. The breadth of service is not what you expect from a mall clinic.

Malls are increasingly looking to wellness and healthcare as a remedy to their e-commerce ailment. They offer advantages that traditional retail cannot:

- Visits are necessary rather than discretionary

- Resistant to online replacement

- Longer dwell times and stable demand

For Healthcare providers, malls are advantageous for equally attractive reasons. They are:

- Centrally located

- Well connected to public transport,

- Already integrated into existing consumer movement patterns, so

that medical visits become

In dense cities like Shanghai, such convenience is invaluable. But, is the Parkway opening an outlier in mall trends, or are such leases becoming commonplace?

WHAT REPLACES RETAIL WHEN SHOPPING GOES DIGITAL

Increasingly, and across global markets, it seems to be a trend. Mall owners are reallocating space away from traditional retail toward healthcare, services, and experience-led uses.

In the UK, Europe’s most digitally penetrated retail market at 31.9%, healthcare and wellness is increasingly being used as an anchor. The shift is clearly visible at Westfield London, where a dedicated Health and Wellness Village that is over 50,000 sq ft includes clinic operators such as Betterview, a laser eye surgery clinic, alongside other medical and wellness providers. The integration of clinics into high-footfall shopping centers reflects the sustained demand for accessible, in person services that are resilient to e-commerce substitution.

WESTFIELD HOW WE SHOP REPORT (2024)

- “52% of UK Shoppers favor wellness hubs over GP clinics

- “66% of Londoners opt for non-emergency healthcare in retail settings including shopping malls”

- “67% of shoppers are interested in access to health services within shopping centers”

In Tokyo, stronger-performing malls increasingly rely on differentiated, experience-driven tenants rather than standardized retail, supporting both footfall and rental performance.

The pattern is consistent. Tenants that meet everyday needs, offer in-person value that cannot be digitized, and encourage repeat visitation are becoming the new mall anchor tenants.

FROM FASHION AND SHOWROOMS TO HEALTHCARE AND EXPERIENCE

BRANDS PULL BACK FROM MALL LOCATIONS

- Zara cut its mainland China store count from a peak of 183 to 69

- H&M reduced its China footprint from 535 stores to just over 300

- Tesla closed roughly 30% of its stores located in core CBD shopping malls

- Nio downsized its NIO House at Oriental Plaza, cutting the car sales area by two-thirds

When this logic is accelerated by extreme digital maturity, we get what is happening in Shanghai: fast-fashion brands and newenergy vehicle showrooms are reducing their mall presence, and medical providers are taking up much of the prime space left empty. Examples include Arrail Dental at Super Brand Mall, RealMed Doctors Group at K11, and Parkway Health at Shanghai Plaza. None of these are peripheral tenants; they occupy visible, high-value space once reserved for traditional anchors.

Experience-led repositioning is also delivering measurable results. Bailian ZX Creative Center, repositioned around anime, comics, and gaming culture, hosted nearly 700 events in 2024. Sales increased by 70 percent year on year, footfall rose by 40 percent, and registered membership exceeded 260,000. These are not branding metrics. They are commercial outcomes tied directly to tenant mix and positioning.

THE FUTURE MALLS WIN BY BEING ESSENTIAL, NOT OPTIONAL

Taken together, the evidence points in one direction. Malls that continue to depend on discretionary retail in a hyper-digital economy will keep losing relevance. Malls that reposition around healthcare, services, and experience-led uses that cannot be replicated online, will stabilize footfall and, in some cases, outperform.

Parkway Health’s clinic is not a novelty. It is not a lifestyle trend. It is a structural response to e-commerce dominance.

The future mall will not succeed by selling more products. It will survive by becoming essential again.